Kenya-Rwanda Fintech Agreement to Boost Cross-Border Payments

Kenya Rwanda Fintech Agreement Signals Regional Integration

The Kenya Rwanda fintech agreement could reshape East Africa’s digital payments sector. Regulators from both countries have signed a memorandum of understanding to develop a licence passporting framework for fintech companies.

The agreement involves the Central Bank of Kenya and the National Bank of Rwanda. It aims to allow digital payment companies licensed in one country to operate in the other without repeating the full licensing process.

This marks a shift toward stronger regional cooperation in financial technology regulation.

A Step Toward a Borderless Fintech Market

Fintech companies currently face barriers when expanding into new markets. They must apply for fresh licences in every country they enter. The process can take months or even years. Companies must also comply with different regulatory systems and requirements.

Under the proposed framework, a fintech licensed in Kenya could operate in Rwanda more easily. Regulators would still supervise companies locally. However, they would recognize each other’s licensing systems.

Industry experts say the agreement could reduce expansion costs for fintech startups.

Why the Agreement Matters for East Africa

The Kenya Rwanda fintech agreement comes as digital payments grow rapidly across East Africa. Kenya has one of the most advanced mobile money ecosystems in the world. This growth has largely been driven by M-PESA, the mobile payment platform operated by Safaricom.

Rwanda has also positioned itself as a regional technology hub. The government has invested heavily in digital infrastructure and startup-friendly policies. By aligning regulatory systems, both countries hope to build a larger market for fintech innovation.

Boost for Cross-Border Payments

Cross-border payments remain a challenge for many businesses in the region. Traders often face delays and higher transaction fees. The Kenya-Rwanda fintech agreement could help fintech companies create payment systems that work across borders.

Such services would allow businesses and consumers to:

- Send money faster

- Pay for goods across borders

- Reduce transaction costs

These improvements could strengthen trade within the East African Community, which promotes regional economic integration.

Uganda’s Economic Growth Faces Budget and Debt Pressures

Uganda's Economic Growth resilient at 6.7% amid weak 62.8% budget absorption, UGX...

Uganda’s Economic Growth Accelerates with Oil Production on Horizon

Uganda's Economic Growth set for 10.4% surge in 2026/27 as oil production...

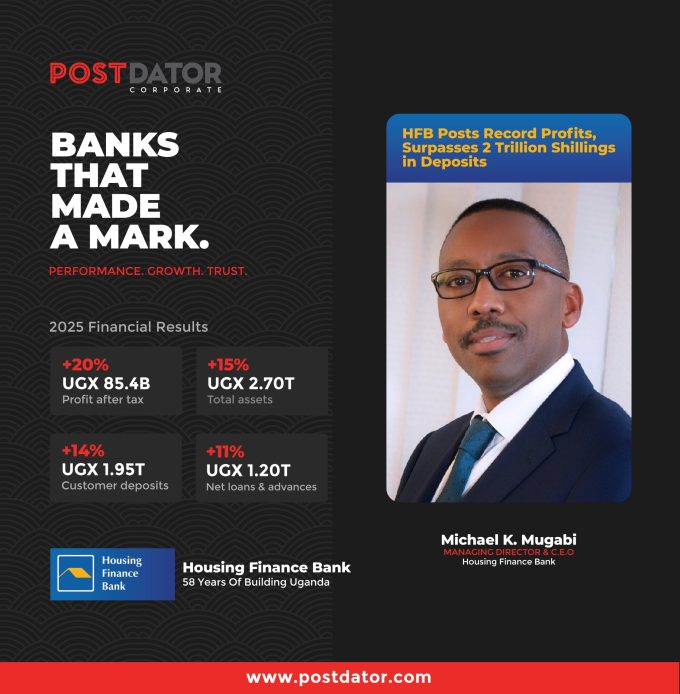

Housing Finance Bank Posts Record Profits, Surpasses 2 Trillion Shillings in Deposits

After 58 years in operation, Uganda’s specialist housing lender delivered its strongest...

“Flex Your Genius”: Students Urged to Think Beyond Class as Stanbic Championship Launches

Participating schools arrived early for the official launch of Season 11 of...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}